Operations

AI in Call Centers

Sample report: Generative AI for Enterprise Call Centres - Strategic Integration, Value Realization, and the Paradigm Shift in Legal Operations

Generative AI for Enterprise Call Centres

Important this is sample report for demo purpose

Executive summary

Generative AI in enterprise call centres is transitioning from “AI as a feature” to “AI as an operating model,” where conversational self-service, agent copilots, automated post-contact work, and machine-driven quality and compliance become default layers across the contact lifecycle. Evidence from a large real-world customer support deployment (5,000+ agents) shows material productivity uplift and heterogeneous impact by skill level, supporting a strong “augmentation-first” investment thesis for large service operations.

From an Investment Committee lens, the most defensible value cases (i.e., those most likely to survive governance scrutiny and deliver repeatable economics) are:

Real-time agent assist (guided knowledge retrieval, next-best action, compliant drafting) paired with strict grounding and guardrails.

Automated summarisation and structured wrap-up (reducing after-call work, accelerating case completion, improving CRM data quality) with explicit accuracy evaluation.

Targeted self-service expansion for high-volume, low-complexity intents, with safe escalation and strong containment analytics.

Risk is non-trivial and increasingly regulated. In the EU, the AI Act is already in force with staged applicability; general-purpose AI obligations apply from August 2025, and additional provisions roll in later. There is also credible reporting of potential timeline adjustments for certain “high risk” obligations, which creates near-term planning uncertainty (enterprises should plan to the published timeline while monitoring changes).

A pragmatic investment posture is “buy a platform, build differentiation”: buy a CCaaS / agent desktop layer with mature telephony, routing, WFM/WEM, and compliance; build a governed GenAI orchestration layer (RAG + tools + evaluation) where differentiated data, workflows, and controls create defensible advantage and reduce vendor lock-in.

Assumptions used in this report

This report is written without constraints on enterprise size, industry, or region; when quantified examples are provided, they are explicitly labelled “illustrative” and intended to show financial mechanics rather than predict outcomes. Regulatory discussion is presented as a cross-region overview with emphasis on the EU and US governance artifacts most frequently used in enterprise risk programs (e.g., EU AI Act timeline; NIST AI RMF and its GenAI profile; ISO AI management/risk standards; OWASP LLM security risks).

Trends overview

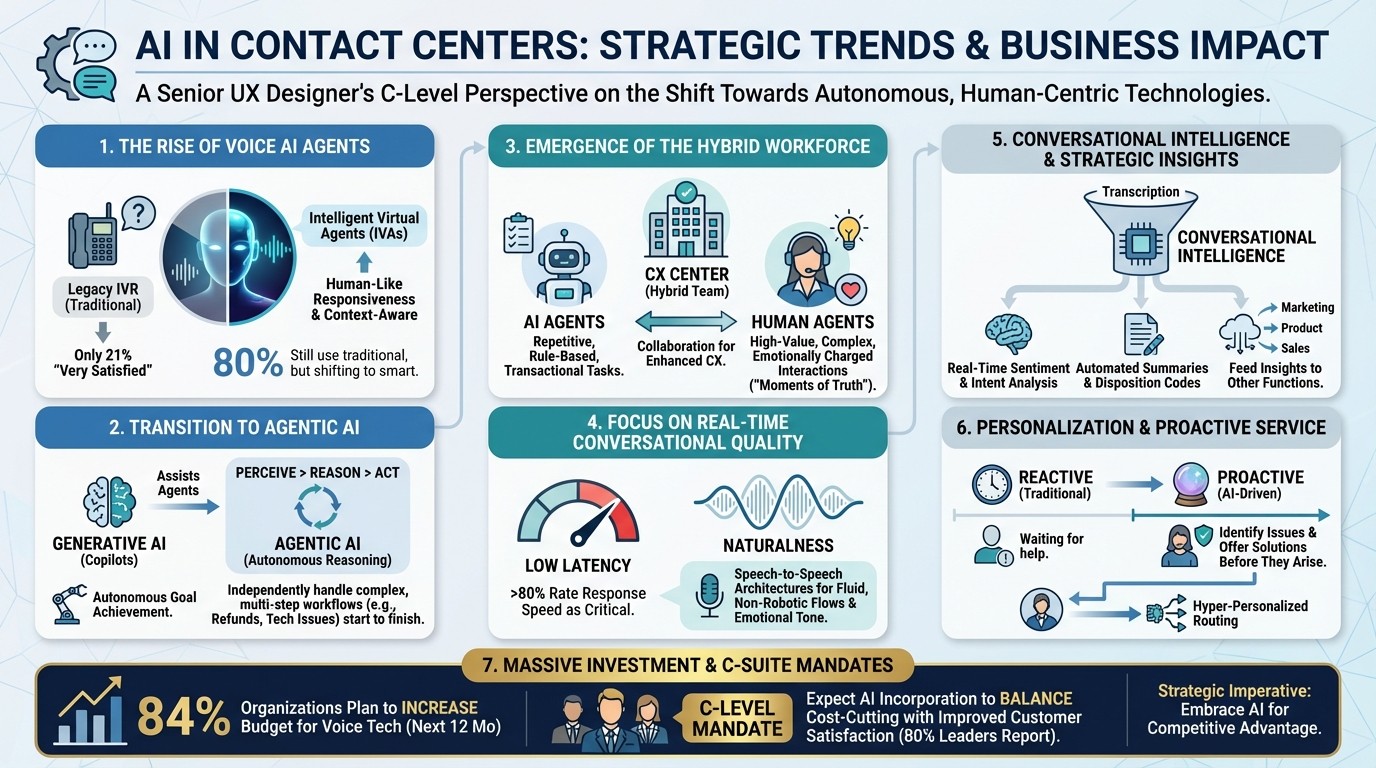

The core trends in call center AI reflect a massive shift from traditional, rigid systems toward autonomous, human-like, and strategically integrated technologies.

1. The Rise of Voice AI Agents. The year 2025 is considered the "year of the voice AI agent," marking a transition from legacy Interactive Voice Response (IVR) systems to sophisticated Intelligent Virtual Agents (IVAs). While 80% of organizations still use some form of traditional voice agent, only 21% are "very satisfied" with them, driving the shift toward systems that offer human-like responsiveness and context-aware conversations.

2. Transition to Agentic AI. AI is evolving beyond simple generative tools that assist agents (copilots) into agentic AI—autonomous reasoning engines that can independently handle complex, multi-step workflows from start to finish. These agents perceive, reason, and act to achieve specific goals, such as processing refunds or resolving technical issues, rather than just generating text.

3. Emergence of the Hybrid Workforce. The traditional call center is being reimagined as a "CX center" operated by hybrid teams of humans and AI agents. In this model:

AI agents manage repetitive, rule-based, and transactional tasks.

Human agents are elevated to handle "moments of truth," focusing on high-value, complex, and emotionally charged interactions that require empathy and creative problem-solving.

4. Focus on Real-Time Conversational Quality. A major trend is the prioritization of low latency and naturalness in voice interactions. Over 80% of organizations rate real-time response speed as a critical feature, as it is essential for creating fluid, non-robotic conversational flows. New "speech-to-speech" architectures are emerging to enable near-instantaneous interactions that preserve emotional tone and intonation without needing to convert speech to text first.

5. Conversational Intelligence and Strategic Insights. Transcription has become "table stakes," and the focus is now on conversational intelligence to extract actionable data from every interaction. Organizations are using AI to:

Perform real-time sentiment analysis and intent detection.

Provide automated call summaries and disposition codes, reducing "after-call work" for human agents.

Feed customer insights directly into other business functions like marketing, product development, and sales.

6. Personalization and Proactive Service. AI is moving call centers from a reactive to a proactive stance. By analyzing historical data and real-time context, AI can identify potential issues before they arise and reach out to customers with solutions. It also enables hyper-personalized routing, where customers are instantly directed to the optimal resource based on their history, sentiment, and current needs.

7. Massive Investment and C-Suite Mandates. Adoption is being fueled by strong financial commitments and executive pressure. 84% of organizations plan to increase their budgets for voice technology in the next 12 months. Furthermore, 80% of CX and contact center leaders report that C-level executives now expect them to incorporate more AI into their operations to balance cost-cutting with improved customer satisfaction.

Market size and growth

Industry estimates consistently show rapid growth in call-centre AI and adjacent cloud contact centre categories, though absolute market size varies by definition (AI-only vs CCaaS platform revenue vs broader customer service software). For example, one market research estimate places the global “call center AI” market at ~$2B in 2024 with growth to ~$7B by 2030, while another estimates ~$2.4B in 2025 and projects growth to the low teens of billions by the mid-2030s.

CCaaS market estimates similarly project strong CAGR into the 2030s, with published figures (methodology-dependent) commonly citing 15–20%+ compound growth.

Importantly, Gartner’s 2026 commentary signals a shift in executive framing: pressure to implement AI is extremely high in customer service leadership, but cost-cutting via automation is not the only (or even primary) objective; customer experience differentiation and proactive service are increasingly positioned as the strategic rationale.

Regulatory and governance shifts

For multinational call centres handling personal data, recorded voice, and regulated workflows, AI governance is moving from “best effort” to “auditable controls.” Key enterprise-relevant shifts since 2020 include:

EU AI Act staged applicability: entered into force August 2024; prohibited practices and AI literacy obligations applicable from February 2025; general-purpose AI model obligations applicable from August 2025; additional timelines extend beyond 2026 for some categories.

Privacy regulators explicitly treat voice interactions as sensitive in certain contexts. The European Data Protection Board highlights that voice data can be biometric and that using voice for identification triggers biometric processing considerations under GDPR.

Standardised risk and security practice is being operationalised through frameworks: NIST AI RMF (2023) and a dedicated GenAI profile (2024) provide a control-oriented structure; OWASP’s LLM Top 10 formalises application-layer risks like prompt injection and insecure output handling; ISO has published AI governance and risk guidance standards that are increasingly referenced in enterprise assurance.

Cybersecurity and AI governance are converging: adversarial ML taxonomies, prompt injection research on RAG systems, and EU cybersecurity guidance increasingly inform “AI security” requirements in enterprise programs.

Major technology advances since 2020

Three technical trajectories materially changed feasibility for enterprise call centres:

Speech foundation models and self-supervised learning improved transcription robustness and reduced dependence on labelled data. Examples include wav2vec 2.0 (2020) and Whisper (2022).

Retrieval-augmented generation (RAG) and tool/function calling enabled “grounded” answers and action-taking over enterprise systems (knowledge bases, CRM, billing, order management), reducing reliance on model parametric memory alone.

Real-time multimodal APIs for low-latency voice interaction matured, enabling speech-to-speech assistants and streaming use cases (relevant for IVR replacement, agent whispering, and real-time compliance cues).

The milestones above are supported by seminal technical publications and official governance sources.

Use cases and value

Core use-case map across channels

Enterprise call-centre automation can be decomposed into four layers:

Customer-facing automation (voice and chat self-service): intent handling, authentication flows, order status, policy lookup, appointment scheduling, and “guided troubleshooting,” with escalation to humans. Vendor platforms increasingly offer “AI agents” that can take actions and then hand off with context.

In-conversation agent assist: real-time transcription, knowledge retrieval, suggested responses, mandatory disclosure prompts, and workflow suggestions (e.g., “open case,” “issue refund,” “schedule technician”).

Post-contact automation: auto-summaries, wrap-up codes, structured disposition, CRM updates, follow-up tasks, and knowledge article drafting. Multiple vendors provide post-contact summarisation in seconds and support passing that output into CRMs.

Quality, analytics, and governance: automated scoring, sentiment, compliance checks, coaching, and evaluation of AI-generated summaries (increasingly formalised via “autoevaluation” or rubric scoring).

These layers map well to the standard CCaaS functional scope (ACD, IVR, predictive dialling, workforce optimisation/monitoring) described by industry definitions.

Quantified value drivers and operational metrics

The most finance-relevant value drivers align to how contact-centre cost is actually incurred:

Productivity and average handle time (AHT): In a large field deployment of a GenAI conversational assistant for customer support agents, productivity increased materially on average, with stronger gains for less experienced agents. This implies predictable capacity unlock if deployed with sufficient adoption and trust.

After-call work (ACW) reduction via summarisation + auto-documentation: Vendors explicitly position summary generation as a way to reduce wrap-up effort and accelerate post-interaction tasks.

Quality / compliance and repeat contact reduction: Better retrieval and structured notes can improve first-contact resolution (FCR) and reduce rework; however, governance must focus on factuality and safe action-taking, as hallucination and prompt injection are known failure modes.

Typical KPI stack for Investment Committee dashboards (measured pre/post and by cohort) should include: AHT and its components (talk time, hold time, ACW), FCR, transfer rate, containment rate (self-service), abandon rate, CSAT/NPS where applicable, compliance exceptions, conversion rate for outbound/sales motions, and cost per contact/resolution. The rationale is that AI impacts both labour minutes per interaction and the probability an interaction resolves without repeats.

Example ROI mechanics

The structure below is intentionally “CFO-auditable”: it converts operational deltas to capacity, then to financial outcomes only with explicit realisation assumptions.

Capacity unlock from AHT improvement

Baseline annual workload hours = annual contacts × average handle time (hours).

Capacity freed (hours) = baseline workload hours × AHT reduction %.

Cash savings = capacity freed ÷ productive hours per FTE × fully-loaded annual cost per FTE × realisation factor.

A real-world anchor for magnitude is the observed productivity uplift in the large customer-support field study (issues resolved per hour up materially, with heterogeneity). Use this as an external “sense check” for whether an assumed 5–15% effective productivity improvement is plausible once adoption is sustained.

Illustrative ROI calculation (not a forecast)

Assume:

5,000 agents; fully-loaded cost $75k per FTE-year (illustrative).

Benefits ramp with adoption; not all capacity becomes immediate headcount reduction (realisation factor).

Program cost includes implementation + subscriptions + operations (illustrative, enterprise-scale).

A worked multi-year financial example is provided in the Financial impact section to show TCO, net benefit timing, and sensitivity dynamics.

Technical architecture

Reference architecture diagram

The architecture reflects current commercial and technical patterns: real-time agent assist and post-contact summaries are common in platform roadmaps; RAG + tool use enables grounded retrieval and action-taking rather than “free-form chat” alone.

Data flows and integration points

Key enterprise integrations to budget and govern:

Telephony/CCaaS and CTI: streaming audio events, call control (transfer, consult), queue/routing metadata, and agent state signals.

IVR / conversational front door: speech-to-speech or speech→text→LLM orchestration; escalation should pass a structured summary + extracted entities/intent and customer context to the agent to avoid “repeat yourself” failure modes described by vendors as a core benefit.

CRM / case management: auto-create and update cases, populate structured fields, attach auto-summaries, and prepare follow-up tasks. Multiple CRM/service platforms document summary generation and agent workflow assistance.

Workforce management and quality: interaction analytics, QA scoring support, coaching insights, and evaluation datasets derived from transcripts and outcomes.

Knowledge and policy repositories: the critical path for grounding, reducing hallucinations, and improving compliance; this is a data-freshness and access-control challenge as much as a modelling challenge.

Model types, deployment, and latency constraints

A production-grade voice stack typically uses multiple model classes:

ASR (streaming), diarisation, language ID.

LLMs / instruction-tuned models for summarisation, drafting, classification, and tool selection.

Embedding models + vector search + rerank (RAG).

TTS (optionally neural) for voice bots.

For voice interactions, latency is a product requirement, not an optimisation. ITU guidance historically notes that keeping one-way delay below ~150 ms supports many applications, and higher delays can be acceptable with engineering care; GenAI voice systems must budget network + ASR + orchestration + retrieval + generation + TTS within a conversational tolerance envelope.

Modern model APIs emphasise low-latency transports (e.g., WebRTC/WebSocket) for voice agents, which can materially affect architecture choices (edge PoPs, regional routing, caching, and partial streaming).

Security, data residency, and observability

Investment-grade deployments require explicit commitments on data usage, retention, encryption, and residency, especially where call recordings or transcripts include sensitive personal data.

Several major GenAI platforms publicly state that business/API data is not used for training by default, with opt-in mechanisms; hyperscaler GenAI services similarly state that prompts/outputs are not used to train underlying base models without customer consent.

Data residency is increasingly a buying criterion; for example, OpenAI has announced data residency options in Europe for business customers, and Google documents “zero data retention” configurations for certain Vertex AI generative services (with required customer actions).

For logging, monitoring, and governance, treat GenAI as a high-risk software subsystem even when the use case is not legally “high-risk”:

Maintain immutable logs of prompts, retrieved passages, tool calls, outputs, and operator overrides (with PII minimisation).

Implement cost controls and abuse detection (model DoS is a documented risk category in OWASP’s LLM security work).

Use systematic evaluation: automated evaluation for summaries is explicitly supported in some agent-assist stacks, and NIST guidance emphasises structured risk management actions for GenAI.

Competition landscape

This section compares major vendors across (a) CCaaS platforms and adjacent enterprise service platforms and (b) open-source building blocks commonly used in “build” strategies. Gartner and Forrester continue to publish flagship CCaaS evaluations (Magic Quadrant / Wave), though access to full scoring is typically restricted; these still shape procurement shortlists and vendor positioning.

Vendor capability matrix

Vendor | Representative GenAI capabilities in call-centre context | Deployment model emphasis | Pricing model signals (public) | Typical strengths | Typical concerns |

|---|---|---|---|---|---|

Genesys | Virtual agents; GenAI-assisted intent creation; conversation summaries; wrap-up code generation; AI-guided interactions | Cloud-first (CCaaS) | Quote/subscription bundles | Mature CCaaS + orchestration narrative | Customisation and governance maturity vary by feature set |

NICE | Auto-summary; agent copilot (suggested responses, summaries); configurable prompts; CRM pass-through | Cloud-first (CXone), enterprise-grade WEM | Quote/bundles | Strong WEM/QM heritage; rich agent assist surface | Controlled-release features and roadmap gating in some areas |

Five9 | “Genius AI” positioning; AI agent assist; AI summaries; engine-agnostic stance | Cloud CCaaS | Bundled plans; “contact sales” | CCaaS with embedded AI bundle packaging | Pricing often quote-based; feature parity differs by tier |

Amazon Web Services | Post-contact summarisation; real-time agent assist; AI agents for self-service with escalation | Cloud-native (AWS) | Usage-based + add-ons typical of hyperscaler | Deep cloud integration; composability; rapid feature shipping | Requires strong in-house architecture/governance to avoid complex sprawl |

Agent assist summaries; customer-experience insights summarisation; summary autoevaluation support | Cloud (GCP) | Consumption/usage typical | Strength in speech + ML tooling; explicit evaluation hooks | Integration effort into heterogeneous CCaaS stacks | |

Microsoft | Copilot summaries for cases and conversations; contact-centre integrations with Teams ecosystem | Enterprise SaaS + platform | Subscription + add-ons typical | Strong CRM/service workflows for enterprises; broad ecosystem | Requires tight data governance; multi-product complexity |

Salesforce | AI-generated work/case summaries; service workflow augmentation | SaaS CRM/service core | Subscription + add-ons typical | Deep CRM footprint; workflow automation | Governance + grounding essential to avoid “bad notes in system of record” |

ServiceNow | Case and chat summarisation; resolution notes generation in CSM | SaaS platform | Subscription | Strong workflow + IT/CSM integration; feedback loops | “Front-office” voice telephony often via partners/integrations |

Cisco | Contact-centre AI assistant: summaries (e.g., dropped call summaries), real-time transcripts | CCaaS/UC integrated | Subscription typical | Strong enterprise comms footprint; continuity features | Feature scope differs across bundles and regions |

Twilio | Agent copilot for Flex; generative highlights and wrap-up notes; API-first orchestration | API-first / composable | Usage + add-on licensing common | Developer-centric flexibility; channel breadth | Requires mature engineering + governance to operationalise at scale |

Talkdesk | GenAI virtual agent (“Autopilot”) for voice/digital; agentic GA milestones | Cloud CCaaS | Published seat pricing entry point | Verticalised automation narratives; quick-start positioning | Vendor claims require validation in comparable KPIs |

Sprinklr | Omnichannel agent assist with real-time guidance across channels | SaaS | Quote/subscription | Strong digital/omnichannel and social heritage | Validate voice depth and telephony integration path |

Interpretation: CCaaS vendors and “hyperscaler contact centres” increasingly converge on a common GenAI feature set (summaries, assist, virtual agents). Differentiation for enterprises tends to come from governance maturity (evaluation and controls), integration depth to systems of record, and operationalisation (rollout + change management + measurement).

Open-source and “build stack” options

Open-source options are rarely end-to-end CCaaS replacements for large enterprises, but they are highly relevant for (a) on-prem / data-residency constrained speech pipelines, (b) building a governed orchestration layer, and (c) avoiding lock-in for retrieval and evaluation components.

Component category | Open-source option (examples) | License / notes | Enterprise fit comments |

|---|---|---|---|

Conversational workflows (NLU/dialogue) | Rasa Open Source | Apache 2.0; commercial “Pro” exists | Good for controlled dialogue + policy flows; GenAI can be integrated but governance is on you |

LLM app/orchestration frameworks | LangChain; LlamaIndex | MIT-licensed (core) | Useful for RAG/tooling scaffolds; must harden for prompt injection + eval |

ASR (local/on-prem) | Whisper; Kaldi; Vosk | Whisper MIT; Kaldi Apache 2.0; Vosk open-source toolkit | Enables on-prem transcription, but requires MLOps, GPU planning, and accuracy benchmarking |

Telephony primitives (self-managed) | Asterisk | GPLv2 dual-licensing | Can underpin legacy/private deployments; not a modern CCaaS equivalent without significant engineering |

Note: “Open weights” model families are sometimes marketed as “open source,” but licensing may not satisfy the Open Source Definition; enterprises should treat model licensing as a compliance workstream, not an implementation detail.

Buy vs Build

The strategic decision: what to buy vs what to build

A high-utility decomposition for Investment Committee decisioning:

Buy:

Telephony reliability, routing, QA/WEM fundamentals, regulatory call recording, and operational features where switching costs are high and differentiation is low. This aligns with how IDC frames CCaaS scope (ACD, IVR, WFO, monitoring).

“Table-stakes” GenAI capabilities that are commoditising (post-call summaries, basic agent assist) if the platform provides strong admin controls and APIs.

Build (or at least own the design and governance):

A policy and orchestration layer that enforces grounding, tool safety, data minimisation, and evaluation across models. Tool/function calling is the enabling mechanism for safe action-taking over enterprise APIs, but it introduces security and integrity risks that require enterprise controls.

Knowledge engineering and retrieval: taxonomy design, document lifecycle, access control, freshness SLAs, and retrieval evaluation. RAG is a canonical approach to improve factuality, but it is not a silver bullet; prompt injection and retriever poisoning are active research areas.

Cost, time-to-market, talent, and maintenance

Time-to-market tends to favour “buy” for the contact-centre core and “build/hybrid” for differentiated workflows:

Vendor platforms provide pre-integrated surfaces (agent desktop widgets, supervisor analytics, packaged summaries), which compress deployment timelines but can constrain model choice and control-plane depth.

Building with open-source/orchestration frameworks accelerates prototyping but shifts responsibility for security hardening, policy enforcement, evaluation, and uptime to the enterprise. OWASP’s LLM risk categories and NIST guidance highlight that these are non-trivial responsibilities.

Compliance and IP posture

For regulated enterprises, buy vs build is also a data-governance decision:

If using external model APIs, the contract + platform controls must align with internal privacy requirements (data retention, training opt-out by default, residency). Public commitments differ by provider and must be validated in procurement and DPIA/TRA processes.

If building on-prem (e.g., self-hosted ASR), enterprises gain data control but take on operational risk, patching, capacity planning, and model lifecycle obligations.

Financial impact

This section provides an illustrative 5-year TCO and benefit model to support Investment Committee discussion. It is not a forecast; parameters should be replaced with enterprise-specific inputs (volumes, wages, occupancy, shrinkage, adoption curves, and procurement pricing).

Illustrative 5-year TCO model and outcome

Illustrative scenario

5,000 agents, fully-loaded $75k per agent-year (illustrative).

Benefits: effective productivity uplift and deflection ramp over time; only a portion becomes “cashable” due to staffing, service level, and redeployment constraints (realisation factor).

Costs: implementation + subscriptions/usage + ongoing operations & governance.

External anchors for feasibility and board-level realism:

Real-world field evidence suggests meaningful productivity gains from GenAI assistance in customer support roles, with heterogeneity by skill level.

Gartner cautions that GenAI cost per resolution can rise and that strategies may shift from pure cost cutting to broader value creation, reinforcing the need for sensitivity analysis and benefit realisation discipline.

Illustrative cashflow table (USD millions)

Year | Cashable benefit ($M) | Program cost ($M) | Net benefit ($M) | Cumulative net ($M) |

|---|---|---|---|---|

2026 | 0.0 | 15.0 | -15.0 | -15.0 |

2027 | 7.9 | 24.0 | -16.1 | -31.1 |

2028 | 24.8 | 23.0 | 1.8 | -29.4 |

2029 | 39.4 | 23.0 | 16.4 | -13.0 |

2030 | 39.4 | 23.0 | 16.4 | 3.4 |

2031 | 39.4 | 23.0 | 16.4 | 19.8 |

Interpretation: In large-scale transformations, payback timing is driven by (a) adoption and trust, (b) the ability to turn capacity unlock into real cost avoidance, and (c) implementation cost management (integration, data foundation, governance). These are precisely the areas that Forrester and Gartner commentary repeatedly flag as the “un-glamorous work” necessary to scale AI in service operations.

Capex vs opex framing

A useful Investment Committee framing:

Capex-like: integration engineering, data/knowledge foundation build-out, security architecture, initial evaluation harness, and change management.

Opex: software subscriptions, model inference consumption, platform support, continuous evaluation, incident response readiness, and ongoing knowledge upkeep.

Because GenAI introduces variable consumption costs, cost governance must be treated as a first-class control (rate limits, caching, routing to smaller models, and guardrails against model DoS).

Sensitivity analysis

Below is an illustrative sensitivity table showing how NPV directionally changes with different effective productivity uplift and benefit realisation assumptions (holding a representative enterprise cost structure constant). This is designed to force explicit debate on “how much productivity is achievable” vs “how much becomes cash.”

Effective productivity uplift → / Benefit realisation ↓ | 50% | 60% | 70% | 80% |

|---|---|---|---|---|

6% | negative | negative | negative | negative |

8% | negative | negative | negative | near break-even |

10% | negative | negative | near break-even | positive |

12% | negative | near break-even | positive | positive |

15% | near break-even | positive | positive | strongly positive |

This structure matches empirical experience: AI projects often fail not because models cannot generate text, but because adoption, workflow integration, and governance are insufficient to deliver durable operational outcomes. Forrester explicitly predicts service quality can dip in the near term as organisations wrestle with deployment complexity.

Risk management

Primary risk categories for enterprise call centres

Data privacy and sensitive data exposure: transcripts and summaries can embed personal data; voice data may be biometric depending on usage (e.g., voice identification).

Hallucination and factuality risk: LLMs can produce plausible but incorrect outputs; this impacts summaries, suggested actions, and customer-facing responses.

Prompt injection and tool abuse: indirect instructions can be introduced through knowledge sources, retrieved text, or user inputs, potentially causing data exfiltration or unauthorised actions; OWASP explicitly ranks prompt injection as a top LLM application risk.

Bias and unfair treatment: model behaviour can differ by language, accent, or demographic proxies in speech and text; this is both a customer fairness issue and an employee-performance management risk if used in QA/coaching.

Regulatory and audit exposure: EU AI Act staged obligations and evolving interpretations require ongoing compliance monitoring; planning uncertainty exists due to public discussion of timeline changes for certain requirements.

Operational resilience: AI availability, latency spikes, and cost blowouts become new failure modes; SLAs must cover not only uptime but also safe degradation (“no AI”), escalation rules, and incident response.

Mitigation controls and testing/validation approach

A robust control stack aligns well to NIST AI RMF + GenAI profile structure (govern, map, measure, manage), while security engineering can be mapped to OWASP LLM risks and adversarial ML guidance.

Key controls that are particularly relevant in call-centre contexts:

Grounding-first generation: require citations to internal policy/KB passages for agent-facing recommendations and customer-facing claims (RAG as default pattern).

Tool safety: enforce allow-listed tools, argument validation, RBAC, step-up authentication for sensitive actions, and “human in the loop” gates for irreversible transactions.

Prompt injection defenses: treat retrieved knowledge and web content as untrusted input; apply content filtering, instruction stripping, and adversarial testing (prompt injection is well-documented and active research continues on attacks against RAG retrievers).

Evaluation harnesses: maintain gold sets for summaries, compliance phrases, and resolution accuracy; use automated evaluation where available and complement with human QA. Google documents summary autoevaluation features for agent assist; this directionally reflects where the market is going.

Privacy-by-design: PII redaction, minimisation, retention controls, and region-aware routing. Several major providers publish “no training by default” positions, but enterprises must still enforce data governance in architecture and contracts.

Incident response, SLAs, and auditability

For GenAI-enabled call centres, incident response must cover both classic security events and “model behaviour incidents”:

Define severity for hallucinated compliance guidance, unsafe actions, or systematic bias in recommendations; maintain rollback capabilities (feature flags) and safe-mode routing (disable GenAI, fall back to scripted flows).

Include adversarial ML and prompt injection in tabletop exercises; NIST provides taxonomy/terminology guidance, and OWASP provides practical risk breakdowns.

Require audit logs sufficient to reconstruct: input, retrieved context, model output, tool calls, and operator override—supporting both compliance audits and root-cause analysis.

View more articles

Learn actionable strategies, proven workflows, and tips from experts to help your product thrive.